Why Everyone Is Talking About Bigger Refunds

[ad_1] IRS data shows average refunds are up, but that doesn’t mean everyone will see the same result. Key takeaways Average tax refunds are trending higher this filing season and filers are expected to see up to $1,000 increase in refund this year. A higher national average doesn’t guarantee your refund will be bigger. Your outcome depends on your income, withholding, and credits. Changes to income, withholding, and credits can all affect your final refund. The news is all abuzz about receiving bigger tax refunds. Refund headlines are everywhere this year. But there’s an important catch if you’re already mentally spending money you haven’t received yet. In general filers could see up to $1,000 increase in refunds or lower balance due this season related to the new tax law changes. Here’s what’s driving the buzz, what people often misunderstand about “bigger refunds,” and how to figure out what your own refund might look like before you file. Are tax refunds bigger this year? So far, yes, on average related to the new tax law changes. The IRS reports average refund figures based on returns processed to date, and those numbers change throughout the filing season as more people submit returns. That’s why bigger refunds this year aren’t guaranteed. Your refund ultimately depends on your own tax situation — including income, withholding, credits, and deductions. Why your refund might be bigger this year Refunds go up for a few common reasons, and they’re usually personal, not universal. For example: Your withholding changed. If more tax was withheld from your paychecks, your refund could be larger, even if nothing else changed. Your life changed. Marriage, a new baby, a home purchase, or childcare costs can shift your credits and deductions. Your income mix changed. Side income, bonuses, or new investments can change what you owe or get back. Some taxpayers may also see differences tied to new provisions associated with the One Big Beautiful Bill Act that the IRS has outlined in its guidance (for example, the car loan interest deduction, as well as deductions tied to tips and overtime for eligible filers). The important part: these changes only matter if they apply to you. Common misconceptions about ‘bigger refunds’ A few ideas show up every year when refund headlines start circulating. Here’s what’s worth keeping in mind. A bigger refund isn’t always “extra money.” A refund is often a sign that you paid more tax during the year than you ultimately owed. If you got a very large refund and would rather have more money in each paycheck, you may want to review your withholding for next year. A bigger refund this year doesn’t mean a bigger refund next year. Refunds can change quickly if your income changes, credits phase in or out, withholding shifts, or tax rules change. One year’s refund isn’t a forecast. The number you expect isn’t always the number you receive. The IRS may adjust returns for errors or missing information, which can change the refund amount and affect timing. If that happens, you’ll typically receive a notice explaining the change. There are exceptions. Some people can still receive a refund even if they didn’t have taxes withheld or aren’t required to file. That’s often because of refundable credits like the Earned Income Tax Credit, which can result in a refund even if you don’t owe taxes. If you’re seeing refund headlines and thinking, “Okay, but what about me?” you’re asking the right question.Get clarity on your refund before you file using the TurboTax Tax Calculator. [ad_2] Source link

What to Do If You Owe Taxes This Year

[ad_1] If you owe taxes when you file your return, pause and breathe. Then, make a plan. Key takeaways Owing taxes one year doesn’t mean you did anything wrong. If you owe more than expected, there are ways to handle it. Filing on time and setting up a payment plan can help you avoid additional penalties. “You owe a couple thousand in taxes.” My CPA — who had undoubtedly delivered that same news countless times in the past — sounded nervous on the other end of the call. When I found out I owed money, my stomach dropped. This felt like a particularly harsh blow, given that I had always gotten money back in the past. However, after a few deep breaths and a helpful talk with the CPA, I figured out a plan that worked for me. If you owe money in taxes, here’s how to get through it. The good news is that owing taxes doesn’t mean you’re out of options. First: Figure out why you owe If you owe money in taxes this year, that usually means something changed with your income or your tax forms. Figuring out what changes caused you to owe money can help you avoid a similar situation in the future. Here are some possible reasons: You earned money that you didn’t pay taxes on throughout the year. You got a raise but didn’t update your tax withholding. A new worker in the family (like a spouse who previously didn’t work and now does) pushed you into a higher tax rate that you didn’t account for. You claimed fewer deductions. You qualified for fewer credits. You had a change in filing status (for example, Married Filing Jointly vs. Married Filing Separately). Next: Figure out a payment plan Finding out you owe taxes can feel overwhelming. The good news is you have options. 1. Pay it off completely. If you have the money to do so (and it won’t completely drain your emergency savings), paying your tax debt in full right away is the best way to put the issue aside and move on. 2. Set up a payment plan. You’re not the first person to owe taxes, and there are payment plan options. If you can’t pay everything at once, the IRS offers payment plans — sometimes spreading payments out over several months or even years. 3. Settle your debt for less. In some cases, the IRS may allow you to settle your tax debt for less than the full amount. 4. Pause collections. If you truly can’t pay your taxes because doing so would keep you from paying other essential bills, the IRS may temporarily pause collections. Keep in mind that this isn’t a get-out-of-jail-free card — your debt will eventually come due. Finally: Take action before the deadline TurboTax professionals can walk you through the different options to help you figure out which one is best for your individual needs. One thing that’s true for everyone: if you owe more than you expected in taxes this year, don’t procrastinate. File your return with TurboTax and set up an IRS payment plan to avoid additional penalties and fees. [ad_2] Source link

I Owed the IRS. Here’s What I Learned About Payment Plans

[ad_1] Key takeaways Owing taxes doesn’t mean you’re in trouble — the IRS offers payment plans that let you spread your balance out over time. Filing on time matters, even if you can’t pay in full, because it can help you avoid additional penalties. When you file with TurboTax, you can request an IRS payment plan directly during the filing process. I sat down to start my taxes when a thought popped into my head: What if I owe this year? I’d picked up a few side gigs and wasn’t setting anything aside for taxes. I started to worry: If it’s a big bill, how would I even handle it? It didn’t help that TikTok is full of worst-case stories about garnished wages and frozen accounts. But here’s what those clips don’t show: owing doesn’t mean you’re in a crisis. In fact, many taxpayers set up payment plans with the IRS every year. How to handle an unexpected IRS tax bill A tax bill can catch you off guard, especially if you’re used to getting a refund. But it’s pretty common — and there are options for paying taxes you owe if you can’t pay right away. Maybe your take-home pay went up, and you didn’t adjust your W-4. Or you picked up freelance work, received a 1099-K for side income, or got a bonus. It doesn’t mean you did something wrong, just that the math worked differently this year, and now you owe. In situations like this, you can: Request an installment agreement from the IRS at the time of filing. Make monthly payments based on what you can afford. Stay in good standing with the IRS as long as you meet their terms. Manageable monthly payments shift the feeling from “What am I going to do?” to “Okay, I can handle this.” Demystifying IRS payment options The IRS offers a few payment plans, but most people choose from two common options: Short-term payment plan This is a helpful option for people who just need a little more time. You have up to 180 days to pay your balance in full, with interest and penalties added. Monthly installment agreement This is what most people mean by an IRS payment plan — monthly payments rather than a single lump sum. If you owe under $50,000, you can usually apply without submitting detailed financial forms. You choose a monthly amount that works for your budget, and approval is often quick. Filing on time can help no matter what Some people wait to file until they have enough money to pay their taxes. But filing and paying are two separate steps. When you file late, the IRS can add a separate “failure-to-file” charge. That fee is usually higher than the late-payment penalty. So even if you need more time to pay, filing on time keeps you compliant and can save you money. Make payments while you plan ahead Setting up a payment plan can bring relief. A monthly amount is something you can budget for instead of scrambling to cover your tax bill all at once. While you’re making those payments, you can also plan for next year: Adjust your W-4 so the right amount of tax is withheld. Set aside part of your side income for taxes as you earn it. Use an estimated tax calculator to get a clearer sense of what you might owe. Handling this year’s tax balance while adjusting for next year helps you feel more in control and less stressed. How to file your taxes with a payment plan If you owe this year, you don’t have to figure out the next step alone. When you file with TurboTax, you can request an IRS installment plan right within the process. You can set up your IRS payment plan in minutes when you file with TurboTax. [ad_2] Source link

I Sold on Poshmark. Do I Owe Taxes on Resale Income?

[ad_1] Key takeaways Selling personal items at a loss usually isn’t taxable, but profits from resale may need to be reported as income. If you regularly resell items for profit, the IRS may treat it as self-employment income. Resale platforms often collect sales tax for buyers, but you’re still responsible for reporting your earnings. I started by cleaning out my closet. A blazer I hadn’t worn in years. Boots that looked great but were impossible to walk in. A bag I bought on sale and never actually used. Listing them on Poshmark felt like a win-win. Less clutter and a little extra cash. By the end of the year, I’d made a few thousand dollars between Poshmark and other resale apps. It felt good to finally get some money back for things I no longer used. Then tax season rolled around, and I started wondering whether that money actually counted as income. Here’s how it works. Selling personal items at a loss usually isn’t taxable If you sell your own clothes, shoes, or accessories for less than what you originally paid, that’s generally not taxable income. For example, if you bought a jacket for $200 and sold it for $75, you didn’t make a profit. You sold it at a loss. Losses on personal-use property aren’t deductible, and since there isn’t any income, it is not taxable. So if you’re mostly reselling items for less than retail, you may not owe income tax on that money. Making a profit makes it taxable Things change if you sell items for more than you paid. Let’s say you grabbed a designer piece at a thrift store and flipped it. When you buy items specifically to resell them for profit, that’s usually considered self-employment. You’ll only be taxed on the profit left over after expenses, which might include: The original cost of the item (cost of goods sold) Platform fees Shipping supplies Packaging materials Mileage to source or ship items It’s not about whether you think of it as a business. It’s about whether you made money, and how much. The $400 profit rule explained If you make $400 or more in profit (income minus expenses) from reselling, you’re required to file a tax return and pay self-employment tax on your earnings. Self-employment tax covers Social Security and Medicare contributions when you don’t have an employer withholding and matching them. You’ll compute that on Schedule SE. That’s often the part casual resellers don’t see coming. Once you cross that $400 profit line, it’s treated like business income. How to report resale app income on your taxes If you regularly buy items to resell for profit, the IRS generally considers that self-employment income. You’ll typically report those earnings on a Schedule C, where you can also deduct expenses like platform fees, shipping supplies, and the cost of the items you sold. Keeping records of what you paid for items and what you sold them for can help you accurately report your profit. How sales tax works on resale apps Income tax and sales tax aren’t the same thing. Income tax applies to the profit you earn. Sales tax applies to the transaction itself and usually depends on where your buyer lives. Most states now have marketplace facilitator laws. That means resale platforms typically collect and send sales tax to the state for you. So in many cases, you don’t have to calculate or collect sales tax yourself; the platform handles it automatically. But since sales tax rules vary by state, it’s still worth checking your state’s department of revenue website to see what applies to you. Why this matters There’s a real difference between clearing out your closet and running a profitable resale side hustle. Knowing where you fall helps you report accurately and avoid surprises later. Selling on Poshmark, Depop, or Mercari? Use our Self-Employment Tax Calculator to estimate what you might owe before you file. [ad_2] Source link

Home office deduction: Do you qualify, and how does it work?

[ad_1] Key takeaways The home office deduction is available to many self-employed filers who regularly and exclusively use part of their home for business. You don’t need a perfect office to qualify, but the space must be used consistently and only for business. Skipping a deduction you qualify for could mean paying more in taxes than necessary. I didn’t skip the home office deduction last year because I didn’t qualify. I skipped it because I was nervous. No accountant. No tax department. Just me, my laptop, and my best friend, Google, late one April evening. If you’re self-employed and doing your own taxes, you probably know the feeling. Every deduction can feel like a judgment call. Every box you check can feel bigger than it should. And somewhere along the way, you may have heard that claiming a home office deduction is “asking for trouble. So you skip it. You move on. You leave money on the table. Why fear feels bigger when you’re filing solo When you don’t have an accountant handling your taxes, everything can feel more exposed. You’re not just filing. You’re translating IRS language, doing the math, and trying not to miss something important. And when a deduction feels even slightly intimidating, it’s easy to default to the “safe” option: don’t claim it. But the home office deduction exists for people who run their business from home, including: Freelancers Consultants Online sellers Coaches Contractors If your home is where you run your business, the IRS recognizes that space costs you something. What actually qualifies as a deduction You don’t need a Pinterest-perfect office to qualify. You need two things. Understanding these requirements is the key to claiming the deduction correctly. Regular use: You use the space consistently for business. Exclusive use: The area is dedicated to business activity only. Principal place of business: The space is where you manage or conduct your work. That’s it. No loopholes. Just documented business use. Why skipping it can cost you If part of your home is used for business, you may be able to deduct a portion of eligible expenses, such as: Rent or mortgage interest Utilities Internet Certain home-related expenses Keeping clear records of these expenses can help ensure your deduction is accurate if questions ever come up. There’s also a simplified option that uses a set rate per square foot, which can simplify the calculation. Either way, the deduction reduces your taxable income. And when you’re self-employed, lowering taxable income can affect both income tax and self-employment tax. Even a modest deduction can make a meaningful difference. The real risk isn’t the deduction For many people, the bigger issue isn’t claiming the home office deduction. It’s paying more than necessary year after year because it feels easier to skip it than to sort through the details. If you’re eligible and you keep reasonable records of your business use, claiming the deduction is simply acknowledging the real costs of running a business from home. Your business has overhead, even if your office is down the hall from your kitchen. The bottom line If you’ve been skipping the home office deduction because it makes you nervous, you’re not alone. But claiming a legitimate deduction doesn’t automatically create problems. If you regularly and exclusively use part of your home for business, you may qualify. The bigger miss is leaving money on the table.See what you may be able to claim with the Self-Employed Tax Deductions Calculator. [ad_2] Source link

Sports Betting Winnings: What to Do at Tax Time

[ad_1] What your winning bet means for your taxes Key takeaways Sports betting winnings are taxable income, even if you don’t get a tax form. Some wins may trigger a form W-2G, but you still have to report all gambling income. Gambling winnings are taxed as ordinary income, added to your other earnings for the year. My favorite football team didn’t even make the playoffs, so when I placed a longshot parlay during the Big Game, it was mostly just to make things interesting. Things got interesting fast: I won, and it was more than I’d ever made on a single bet before. After the excitement wore off, one question hit me: Did I need to report that money on my taxes? If you’ve ever had that same question after a winning bet, here’s what to know. Your winnings are considered income The IRS considers gambling winnings to be taxable income. Whether you win through a sports betting app, at a casino, on a scratch-off ticket, or somewhere else, that money generally needs to be reported on your tax return. Whether it’s $5 or $5,000, winnings count as taxable income. Depending on the size and type of your win, you may receive Form W-2G. For some gambling winnings, this form is issued when the payout meets IRS reporting thresholds. In some cases, federal taxes may also be withheld from larger winnings. Even if you don’t get a W-2G form, you’re still responsible for reporting all gambling income. How your gambling winnings are taxed Gambling winnings are generally taxed as ordinary income. That means they’re added to your other income for the year, such as wages, self-employment income, or investment income. If you itemize your deductions, you may be able to deduct gambling losses up to the amount of your winnings. But you can’t deduct more in losses than you won, and you’ll need records to support your claim. Report your winnings confidently when you file It may sound complicated at first, but the basics are simple: report your winnings, keep good records, and understand when losses may be deductible. Tools like TurboTax can help guide you through reporting gambling income and losses step by step when you file. Betting regularly? Here’s how to report gambling winnings and losses the right way. [ad_2] Source link

Last-Minute Tax Filing and Extension Guide

[ad_1] Tax day has a way of sneaking up on everyone. Whether you still haven’t started, or just need more time, you have more options than you think, and the worst thing you can do is nothing. Don’t let tax season overwhelm you. We’ve rounded up everything you need to know about tax deadlines and extensions, so you can stop stressing and start taking action. A note about mailing your tax return If you plan to mail your tax return or payment, you should know that a recent processing clarification by the U.S. Postal Service could affect whether the IRS considers your tax return or payment on time, even if you mailed it before the deadline. The IRS uses the postmark date on your envelope and not the date you drop it in the mail to determine if you filed on time (known as the “mailbox rule”). With USPS processing changes, the postmark stamped on your envelope may reflect the date processed at the sorting facility which could be later. To protect yourself, consider requesting a hand-stamped postmark directly at a post office retail counter when you mail anything tax-related. The safest approach is to send payments and tax returns electronically. If you have to use mail, send your payment or tax return well ahead of any deadline. You can also request a certified return with a signature so you have proof that the IRS received your payment or tax return. Ready to file? Go from zero to done, fast The hardest part of filing your taxes is usually just starting. Whether you’ve been putting it off, you’re filing for the first time, or you just want to make sure you’re doing this right, you’re in the right place. These three articles walk you through everything you need before you sit down, answer the questions most filers ask first, and help you move from overwhelmed to done as quickly as possible. “De-Stress Tax Time: The 6 Top Filing Tips Everyone Should Know” Anxiety about taxes is real, and it stops a lot of people from filing on time. This article (with video) cuts through the stress with six practical tips that apply to almost every filer, regardless of your income or how complicated your situation is. First: De-stress “Tax Documents Checklist: How to Win Big This Tax Season” Select the life events that applied to you and we will create a tax document checklist made especially for your unique situation. You can come to TurboTax and fully hand over your documents over to a TurboTax Live tax expert and get your taxes done from start to finish. Use the tax documents checklist “Can You File Taxes on Your Phone?” Yes! Mobile tax filing has become increasingly popular. Mobile tax filing offers convenience, speed, and security, making it easier to prepare and submit your return from anywhere. Read the mobile tax filing tips Learn about tax deadlines Not ready to file by April 15? That’s okay, filing an extension is quick, free, and gives you until October to submit your return. And if you’ve already filed and realized something isn’t right, the IRS has a straightforward process for fixing it. Either way, taking action now is always better than waiting. Here’s what you need to know. “What Day Are Taxes Due? File by the April 15 Deadline or Get an Extension” Not sure when your taxes are actually due? This article covers the federal tax deadline, what to do if you can’t file or pay on time, and how to handle everything online. So you have a clear picture of exactly where you stand and what your next move should be. Learn about the tax filing deadline “What Happens if You File Your Taxes Wrong“ Worried about the fallout from filing late or making a mistake? This breakdown explains how the IRS calculates failure-to-file penalties, failure-to-pay penalties, and interest charges, and importantly, how to minimize the damage if you’re already behind. Learn how to minimize the damage “How To File an Extension Online with TurboTax” An extension gives you six extra months to file your return, but it doesn’t give you extra time to pay what you owe. This guide walks you through exactly how to request more time from the IRS, what the extension actually covers, and what you still need to do by April 15. Learn about filing an extension “IRS Form 4868: A Step-by-Step Guide To Filing an IRS Tax Extension“ Form 4868 is the official form you file to request a federal tax extension. If you’ve never done it before, this article makes it straightforward, walking you through each field, the filing deadline for the form itself, and how TurboTax can help you file it in minutes. Get the guide for filing an extension We’ve got you If you need more time, an extension is there for you. If something went wrong, it can be fixed. And if you’re just getting started, the hardest part is already behind you. Taxes don’t have to be overwhelming, and no matter where you are in the process, there’s always a clear next step. TurboTax is here to help you get it done with confidence, whatever that looks like for you. [ad_2] Source link

Get Expert-Backed AI Tax Help with TurboTax on Claude and ChatGPT

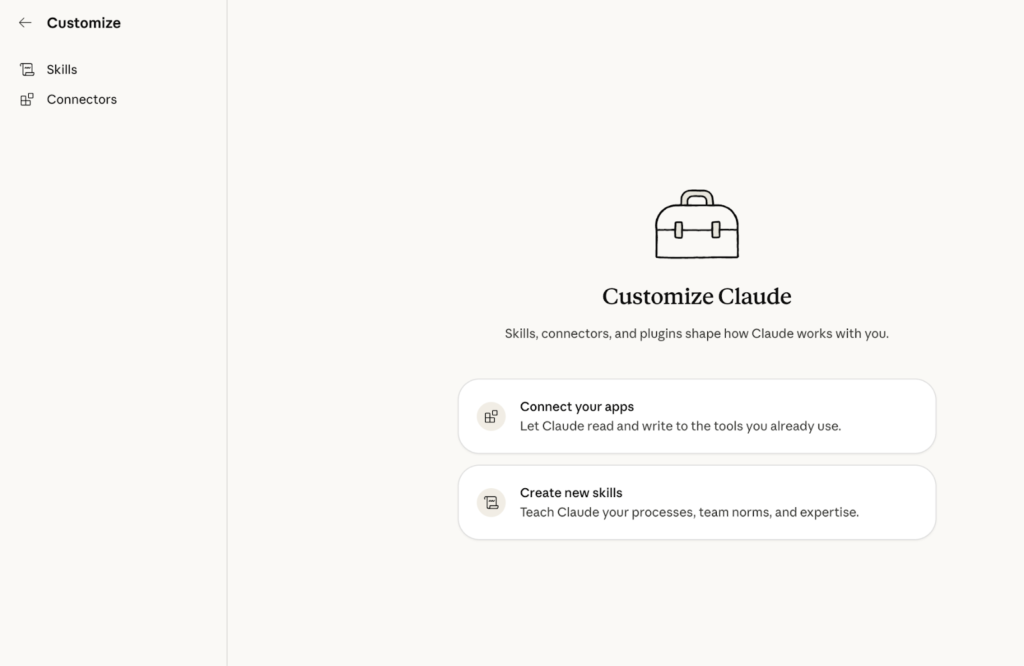

[ad_1] Your tax questions deserve expert-backed AI Tax season has always come with one big question: Am I leaving money on the table? This year, with AI rapidly reshaping how people manage their finances, a second question has emerged: Can I trust AI with something this important? Our answer is simple: Yes, you can trust AI with your taxes … when it’s backed by decades of tax expertise and purpose-built, for one of the most consequential financial moments of the year. Nearly 40 million Americans trust TurboTax to do exactly that, we’re bringing that trusted experience to more places, and making it more robust than ever before. Today, we’re proud to announce two milestones that bring TurboTax’s trusted financial intelligence to more customers, wherever they already are. The tax engine behind millions of returns, now live on Claude The TurboTax connector on Claude brings TurboTax capabilities directly into Claude, including personalized and real-time tax estimates, instant refund projections, seamless connection to a live Intuit tax expert, and a personalized tax document checklist with in-app document capture capabilities. This brings TurboTax’s trusted tax engine — the same core framework that powers millions of returns every year — directly into Claude, the AI assistant millions of people already use for work and life. And the data collected by TurboTax stays protected with the same privacy and security practices we apply across all of our products. How to launch the TurboTax Claude Connector In three simple steps, you can add TurboTax to your Claude account: Step 1: Open your Claude.ai account and navigate to the left side tab, “Customize.” Step 2: Click “Connectors,” then click on the search bar and type “TurboTax.” Select the TurboTax app from the results. Step 3: Click “Connect” and start asking your tax questions. The TurboTax app in ChatGPT just got even better Since launching our app in ChatGPT earlier this year, TurboTax has been helping users get personalized tax estimates, instant refund projections, and connect seamlessly with a live, local tax expert. Today, that experience gets even better with help for one of the biggest friction points in filing: getting organized. Based on a few questions about their tax situation — whether they’re a freelancer, a homeowner, a retiree, or all three — users receive a personalized checklist of which forms to gather, can upload documents directly within the TurboTax app in ChatGPT, and can pick up right where they left off in TurboTax to continue filing. How to get a personalized tax checklist in ChatGPT Step 1:In ChatGPT, find Apps in the left side tab. Search for “Intuit TurboTax” and click “Connect Intuit TurboTax.” Step 2: You’ll be prompted to sign into TurboTax or set up an account, if you don’t already have one. You’ll be brought back to ChatGPT after logging in. Step 3: From the Intuit TurboTax App, click “Start chat.” Step 4: Try a prompt like “Help me gather the documents I need for my taxes.” Step 5: Answer a few questions about your tax situation and get your personalized checklist. Review your checklist, gather your documents, and start filing on TurboTax. This is what purpose-built AI actually looks like People are increasingly turning to AI to help manage their most important financial decisions. For the 75% of American households earning under $100,000, the tax refund is often the largest paycheck of the year: The average refund last season topped $3,000, and filers this season expect to see up to a $1,000 increase in their refund or a lower balance due. When this much is on the line, you need accuracy you can count on. TurboTax knows your financial picture, operates on a platform built to protect your data, and has a real expert standing behind every calculation: purpose-built and trained by our network of 15,000 tax experts, leveraging 70,000 financial data points per consumer on a closed, secure platform. What TurboTax customers get that no one else can offer Your return, nearly done before you start. Our AI in TurboTax automates data entry for 90% of tax forms, including complex 1040s and 1099 composites, by ingesting them directly from financial institutions. For simple filers, we can prepare 80% of your return before you even start. More money back in your pocket. Our Cost Basis Adjustment Assistant alone saved customers an average of 50 clicks and lowered taxable income by a median of $12,000 during its pilot phase. Tax Break Finder identifies missing credits and deductions customers may qualify for. In a pilot, Tax Break Finder found additional deductions or credits for 12% of filers who reported an average savings of $327. Your refund, faster. Getting your refund is important; getting it quickly is just as critical. TurboTax’s 5 Days Early lets eligible filers receive their federal refund up to 5 days earlier in their bank account of choice for a fee, or in a Credit Karma Money Checking account for no additional cost. And with Refund Advance, qualifying customers can access up to $4,000 of their expected refund with no loan fees and 0% APR — in as little as 30 seconds after IRS acceptance of your tax filing. Putting every dollar to work. Getting the refund is just the start. Intuit’s Consumer Platform, which combines TurboTax and Credit Karma, uses AI to help members take control of their finances year-round. Credit Karma’s Refund Assistant provides members with personalized refund allocation plans. AI and human intelligence, working together for you. Our AI and proprietary technologies do the heavy lifting: automating, calculating, and personalizing while our network of 15,000 experts provide the judgment, confidence, and accountability that only a human can bring. Together, these milestones are the latest chapter in Intuit’s long-standing commitment to AI leadership. Backed by decades of investment in data and AI, Intuit has moved quickly and deliberately to bring that expertise into the platforms where people are already getting work done. Partnering with the world’s leading AI companies ensures that when people turn to AI for financial guidance,

A Guide to Taxes on NIL Income

[ad_1] Key takeaways NIL income is usually taxable at both the federal and state level, depending on where you earn it. Non-cash compensation relating to NIL deals, like free merchandise or trips, is also considered taxable income. Where you live, play, and sign deals can all affect your final tax bill. I was talking to a college athlete friend who’d just landed her first NIL deal. It was a huge win for her. Extra money, more visibility. But before she could celebrate, she’d been up Googling taxes at midnight, trying to work out how much money she’d be keeping. It’s a lot to process, especially if you’re new to paying tax. Between different rules and different taxes, the math can get complicated fast. The good news is that understanding how it applies to you will help make it less overwhelming. NIL income and why taxes can reduce how much you keep NIL (name, image, and likeness) income comes from deals and opportunities student athletes get based on their personal brand. Whether it’s an actual payment in dollars or non-cash compensation in the form of merchandise or trips, the IRS treats it as taxable income. That means NIL earnings are likely to be subject to: Federal income tax Self-employment tax Whether they’re subject to state income tax as well depends on the circumstances. To understand how it all works, it’s worth starting with the basics. NIL taxes FAQ Do I have to pay state taxes on NIL income? In most cases, yes. Though there are some places that don’t have state income tax, in most states NIL income is taxed in the same way as wages and freelance income. Do NIL deals count as self-employed income? Yes. The IRS generally considers NIL income as self-employed income, so earnings of at least $400 for the year (after deductions) are subject to federal self-employment tax of 15.3%. States assess income tax on these earnings. If you expect to owe $1,000 or more, the IRS recommends making quarterly estimated payments using Form 1040-ES. Does it depend on where I live and play? Yes. And this is where it can get complicated. Unless you live in a state that doesn’t tax income, you’ll likely be taxed by your home state. If you earn money tied to another state, you may need to file in more than one state and claim credits (or allocate taxes) to avoid being taxed twice. Should I report NIL earnings when I file? Yes. Your NIL income should be reported on Schedule C when you file a Form 1040. You may receive a 1099 form to report the income, but it’s important to report all earnings even if you don’t receive a 1099. What if I’m an international student earning NIL income? If you’re an international student, you may be eligible to receive NIL income, and you’ll have to pay U.S. taxes on that income.Your filing requirements will probably vary, depending on your status. It’s worth checking your specific situation and what it might mean before you start earning to avoid falling foul of the rules. Understanding taxes on NIL income NIL deals can be a big financial step, especially if you’re able to keep more of what you earn. Planning ahead can help you avoid giving more away than necessary, and that money can stay in your pocket as a head start for your future. See what you may be able to claim with the Self-Employment Calculator and get a clearer picture of your NIL taxes before filing your tax return. [ad_2] Source link

Hello world!

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!