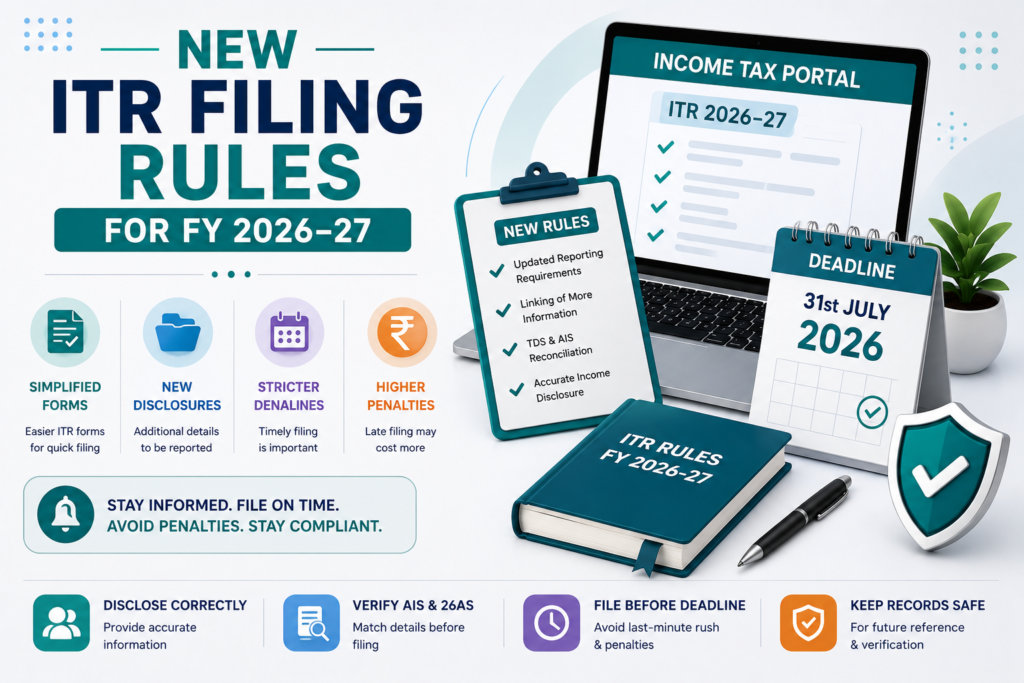

New ITR Filing Rules for FY 2026–27 Every Taxpayer Should Know

TL;DR Income earned between 1 April 2026 and 31 March 2027 is governed by the Income-tax Act, 2025. This period is officially referred to as Tax Year 2026–27 under the new framework. The return for this income will generally be filed in 2027 using new ITR forms prescribed under the Income-tax Rules, 2026. The most important points taxpayers should know are: The Income-tax Act, 2025 applies from 1 April 2026. “Previous year” and “assessment year” are replaced by the simpler “tax year” concept for current income. Taxpayers must use new section references for income, deductions and TDS. Final ITR forms for Tax Year 2026–27 must be checked once officially notified. Non-audit business taxpayers may receive a different filing deadline from ITR-1 and ITR-2 taxpayers. Revised returns have a longer correction window under the new framework. Updated returns remain available subject to restrictions and additional tax. AIS, TIS, Form 26AS, bank interest and capital-gains data must be reconciled before filing. First, Understand the FY, AY and Tax Year Difference Taxpayers often confuse FY 2026–27 with AY 2026–27. They are not the same. Term Income Period Filing Period AY 2026–27 Income earned in FY 2025–26 Return filed during 2026 Tax Year 2026–27 Income earned from 1 April 2026 to 31 March 2027 Return generally filed during 2027 The return currently being filed in 2026 relates to income earned up to 31 March 2026 and remains governed by the Income-tax Act, 1961. Income earned from 1 April 2026 onwards falls under the Income-tax Act, 2025. This distinction is important because the applicable Act, section references, forms and filing framework are different. The Income-tax Act, 2025 Now Governs Current Income The Income-tax Act, 2025 came into effect on 1 April 2026. One of its main objectives is to simplify the structure and language of Indian income-tax law. Instead of using separate terms such as “previous year” and “assessment year” for current income, the new Act uses the term “tax year”. For taxpayers, the transition means: New section numbers New ITR forms New rule references Revised payroll and TDS mapping Updated tax-software configurations Concurrent operation of old and new compliance systems The old Act has not disappeared completely. Returns, revisions, notices and assessments relating to income earned before 1 April 2026 continue under the Income-tax Act, 1961. What Has Changed for Taxpayers in FY 2026–27? 1. New Act and New Section Numbers Taxpayers will notice that familiar provisions now appear under different section numbers. For example, deductions historically associated with Chapter VI-A or familiar sections such as Section 80C may be referenced through different sections and schedules under the Income-tax Act, 2025. This does not automatically mean every deduction has disappeared. It means taxpayers, employers, payroll teams and tax professionals must use the correct new-Act references. Tax-saving declarations submitted to employers for salary earned from April 2026 should therefore follow the new legal framework. 2. New ITR Forms Will Apply Income earned during Tax Year 2026–27 will be reported through ITR forms prescribed under the Income-tax Rules, 2026. The familiar ITR categories may continue in a revised format, but taxpayers should not assume that the disclosures, schedules or eligibility conditions will remain identical. The final form should be selected only after checking: Residential status Salary or pension income Number of house properties Capital gains Business or professional income Presumptive income Foreign assets or foreign income Directorship or unlisted shares Agricultural income Income taxable at special rates Taxpayers should avoid preparing their return using last year’s assumptions. 3. Filing Deadlines May Differ by Category One important policy direction for Tax Year 2026–27 is the separation of due dates for different non-audit taxpayers. Individuals eligible to use simpler individual-return forms, such as ITR-1 or ITR-2, are expected to continue with the standard July timeline. Non-audit business taxpayers may receive an August deadline under the new framework. This could provide additional time to finalise business accounts without delaying simple individual returns. However, the exact deadline applicable to a taxpayer should be verified when the government publishes the relevant return forms, rules and filing calendar for 2027. Do not assume that every non-audit taxpayer has the same due date. 4. Longer Window for Revised Returns A revised return allows a taxpayer to correct an omission or incorrect statement in an original or belated return. The new framework extends the revised-return timeline from nine months to twelve months from the end of the relevant tax year. This can give taxpayers additional time to correct errors, particularly where a belated return is filed close to the end of the original correction window. A fee may apply when a revised return is filed beyond the earlier nine-month period. Taxpayers should therefore correct known errors as soon as possible rather than treating the extended window as the normal filing timeline. 5. Updated-Return Framework Continues An updated return provides an additional opportunity to disclose omitted income after the normal original, belated or revised-return windows have closed. Under the new framework, an updated return may generally be available within the prescribed extended period, subject to conditions. An updated return cannot ordinarily be used simply to: Reduce tax liability Increase a refund Create an artificial loss Claim a benefit after withholding income earlier Additional tax increases depending on how late the updated return is filed. The framework also allows certain updated-return corrections involving a reduction in an earlier reported loss. Special rules may apply where reassessment proceedings have begun. An updated return is therefore a voluntary-compliance mechanism, not a low-cost replacement for accurate filing. 6. TDS Reporting Moves to the New Act Salary and other income arising from April 2026 are governed by the new Act’s TDS provisions. Employers and deductors must update: Payroll calculations Investment declarations Deduction references TDS certificates Accounting software Return-mapping systems Employees should check whether their employer has correctly considered: Chosen tax regime Eligible deductions Previous-employer income Other declared income Tax already deducted Perquisites and allowances A mismatch at payroll stage can result in excess tax, short deduction or a year-end

GST Department’s Growing Use of AI: How Businesses Can Stay Compliance-Ready

TL;DR GST compliance is increasingly driven by connected data rather than isolated return filing. The GST ecosystem can compare information across outward-supply returns, tax payments, purchase data, input tax credit, e-invoices, e-way bills and taxpayer history. AI and advanced analytics make it easier to identify unusual patterns, repeated mismatches and transactions that require further verification. For businesses, this does not mean that every mismatch proves wrongdoing. Genuine timing differences and clerical errors can occur. However, companies must be able to identify, document and explain them. The safest approach is to: Reconcile GST data every month Validate invoices before filing Monitor vendor compliance Review input tax credit eligibility Match e-invoices and e-way bills with books Maintain supporting documents Conduct periodic CA-led GST reviews GST Scrutiny Is Becoming More Data-Driven GST compliance has moved far beyond the days when authorities depended primarily on manual inspection of individual returns. Today, large volumes of digital information are generated through: GST registrations GSTR-1 GSTR-3B GSTR-2B E-invoices E-way bills Tax payments Refund applications Amendments Supplier and customer filings These systems create connected data trails. When one business reports a B2B sale, that information affects the recipient’s purchase and input tax credit records. When an e-invoice is generated, its invoice number, taxable value, GST rate and recipient details can be compared with return data. When goods move under an e-way bill, the movement record can be compared with invoices and reported turnover. As analytical capabilities improve, businesses can no longer treat each GST return as a separate compliance task. Every filing must tell a consistent story. What AI in GST Compliance Actually Means AI in GST compliance does not necessarily mean that software independently decides whether a taxpayer is guilty of non-compliance. In practice, AI, machine learning and advanced analytics may assist the system in: Identifying unusual filing patterns Comparing large datasets Highlighting high-risk transactions Detecting abnormal ITC behaviour Finding invoice-network relationships Prioritising cases for verification Identifying repeat mismatches Monitoring changes in taxpayer behaviour A risk flag may lead to further verification. The business must then provide records, reconciliations or explanations. This distinction is important. An anomaly is not always a violation. But an unexplained anomaly can become a compliance problem. Data Sources That Can Be Cross-Checked A modern GST review may involve more than one return. Data Source Possible Comparison Sales register GSTR-1 and e-invoice data GSTR-1 GSTR-3B outward-tax liability Purchase register GSTR-2B and vendor invoices E-invoice records GSTR-1 and books E-way bills Invoices, dispatch records and turnover Credit notes GSTR-1 amendments and customer records Bank records High-value receipts and reported sales Vendor filings Recipient’s ITC claims Tax ledgers Liability discharged through cash and credit Annual financials Aggregate turnover reported under GST Businesses should therefore maintain consistency not only within GST returns but also between GST records and financial accounts. Compliance Patterns That May Attract Attention GSTR-1 and GSTR-3B Differences GSTR-1 reports outward supplies, while GSTR-3B records the summary liability and tax payment. Differences can arise because of: Missed invoices Wrong reporting periods Incorrect amendments Credit-note errors Classification mistakes Manual data-entry errors Incomplete e-invoice integration A small timing difference may be explainable. A recurring or material difference requires immediate review. Businesses should reconcile outward supplies before filing GSTR-3B instead of relying only on auto-populated values. Unsupported or Irregular ITC Claims Input tax credit is one of the most closely monitored areas under GST. Potential concerns include: ITC claimed without invoice reflection Duplicate credit Credit on blocked expenses Vendor GSTIN mismatch Credit claimed in the wrong period ITC retained despite supplier-related issues Credit claimed without receipt of goods or services Missing proof of payment or business use A business should not assume that an invoice in its accounting software automatically establishes ITC eligibility. Eligibility, document validity, supplier reporting and the nature of the expense must all be reviewed. E-Invoice and Return Mismatches Where e-invoicing applies, businesses must ensure that invoice data generated through the Invoice Registration Portal matches: The invoice issued to the customer Accounting records GSTR-1 Credit or debit notes E-way bill data, where relevant Common problems include: Wrong customer GSTIN Incorrect taxable value Duplicate document numbers Wrong place of supply Cancelled e-invoice not updated in books Invoice booked in a different return period Manual invoice issued without a valid IRN A controlled invoice workflow is therefore essential. E-Way Bill and Turnover Inconsistencies E-way bills create a digital trail for the movement of goods. Possible inconsistencies include: Significant e-way bill movement but low reported turnover Invoice value differing from e-way bill value Repeated cancellation patterns Goods movement without corresponding sales entry Incorrect vehicle or consignee information E-way bill generated under the wrong GSTIN Businesses dealing in goods should reconcile e-way bills with dispatch registers, invoices and GSTR-1. Unusual Vendor or Transaction Patterns Analytics can examine relationships across suppliers and recipients. Patterns that may require further explanation include: Large purchases from newly registered suppliers Sudden increase in ITC claims Repeated dealing with non-compliant vendors Circular-looking transaction patterns High credit claims relative to business activity Purchases inconsistent with the nature of the business Multiple suppliers sharing unusual common characteristics This makes vendor onboarding and periodic vendor review part of GST risk management. Repeated Amendments and Late Corrections Corrections are permitted within the GST framework, but frequent amendments may indicate weak internal controls. Repeated corrections can arise from: Incomplete monthly closing Poor invoice validation Wrong GSTIN capture Misclassification of supplies Late receipt of information Dependence on manual spreadsheets Rather than treating amendments as a routine solution, businesses should identify the root cause and improve the process. How Businesses Can Become Compliance-Ready 1. Build an Invoice-Level Control System GST accuracy begins before return filing. Every invoice should be checked for: Supplier or recipient GSTIN Invoice number and date Place of supply HSN or SAC Taxable value GST rate CGST, SGST or IGST treatment Reverse-charge applicability E-invoice requirements E-way bill requirements Use maker-checker controls for high-value or unusual transactions. 2. Reconcile GST Every Month A monthly GST closing should compare: Books vs GSTR-1 GSTR-1 vs GSTR-3B Purchase register vs GSTR-2B

Why More Indian SMEs Are Choosing Virtual CFO Services Instead of Hiring Full-Time Finance Teams

TL;DR Why SMEs Are Moving Towards Virtual CFO Services Many Indian small and medium-sized enterprises have outgrown basic bookkeeping but are not yet ready to bear the cost and complexity of building a complete in-house finance department. Virtual CFO services address this gap by giving SMEs access to experienced financial leadership on a flexible or part-time basis. A Virtual CFO can help a business with: Cash-flow planning Budgeting and forecasting Management information systems Profitability analysis Working-capital management Financial controls Lender and investor reporting Tax and compliance coordination Strategic financial decision-making The model can be particularly valuable for growing businesses that need better financial visibility but do not require a senior finance executive at the office every day. However, a Virtual CFO is not simply a remote accountant. Bookkeeping records transactions. A Virtual CFO interprets those records and helps management decide what to do next. What Are Virtual CFO Services? Virtual CFO services provide businesses with access to Chief Financial Officer-level guidance without requiring them to appoint a full-time CFO or immediately build a large internal finance department. The word “virtual” does not mean that the service is entirely automated or handled only through software. It usually means that the financial expert works with the business on an outsourced, part-time or hybrid basis. Depending on the scope, a Virtual CFO may work with: The business owner Internal accountants Bookkeepers Tax consultants Department heads Bankers Investors Auditors Legal and compliance professionals The Virtual CFO examines the financial information generated by these functions and converts it into management insight. For example, instead of merely reporting that receivables have increased, the Virtual CFO may identify: Which customers are delaying payments How the delay is affecting working capital Which invoices need immediate follow-up Whether credit terms should be revised How much cash may be available over the next 13 weeks This strategic interpretation separates CFO support from routine accounting. Why Financial Management Becomes More Complex as SMEs Grow A small business may initially operate with basic accounting software, one accountant and direct involvement from the owner. That structure may work when: The transaction volume is low The business has a small customer base Payments are predictable The owner approves every expense Inventory is limited There are few employees or branches Growth changes the financial environment. As an SME expands, it may need to manage: More customers and vendors Multiple bank accounts Employee reimbursements Inventory across locations Longer customer credit periods Business loans and repayment schedules GST and TDS obligations Department-level budgets New branches Capital expenditure Investor or lender reporting Product-wise profitability Working-capital pressure India’s MSME sector contributes approximately 30% of the country’s GDP and more than 45% of exports, making better financial management within the sector economically significant. The Economic Survey 2025–26 also described MSMEs as a backbone of India’s industrial economy. As these businesses become more formal and growth-oriented, their financial requirements extend beyond filing returns and maintaining ledgers. The problem is that many SMEs reach this stage before they can justify a complete senior finance team. Virtual CFO vs Accountant vs Full-Time Finance Team These three functions are related, but they are not interchangeable. Financial role Primary responsibility Accountant or bookkeeper Records transactions and maintains books Tax or compliance professional Handles returns, filings and regulatory requirements Virtual CFO Interprets financial data and advises management Full-time CFO Leads finance strategy as an internal senior executive In-house finance team Manages daily accounting, reporting, treasury and controls An SME may still need an accountant after hiring a Virtual CFO. In many cases, the Virtual CFO works with the existing accountant instead of replacing that person. The key difference lies in the questions each role answers. An accountant may explain: What was recorded? What amount is payable? Which return must be filed? Which invoice remains outstanding? A Virtual CFO should also help answer: Why has the gross margin declined? Can the business afford a new branch? How much working capital will be required? Which products or customers generate the strongest contribution? Will the company face a cash shortage in three months? What financial information will a lender or investor require? Why Indian SMEs Are Choosing Virtual CFO Services 1. Lower Fixed Employment Costs Building a complete internal finance function involves more than one salary. A business may need to account for: Recruitment costs Senior finance salaries Employee benefits Payroll taxes Office infrastructure Finance software Training Supervision Replacement costs Additional accounting and reporting staff A Virtual CFO model allows the business to purchase an agreed level of financial expertise based on its current requirements. The engagement may be structured around: A fixed monthly retainer Defined deliverables A specified number of review meetings A temporary growth or restructuring project Fundraising preparation Cash-flow intervention Periodic financial oversight The precise fee varies significantly according to transaction volume, business complexity, locations, reporting needs and the provider’s involvement. The relevant comparison should therefore be based on the scope and outcomes, not merely the monthly fee. 2. Access to Senior Financial Expertise Many SMEs can hire a junior accountant but cannot immediately justify a senior professional experienced in: Financial planning Working-capital management Business modelling Banking negotiations Internal controls Cost analysis Board reporting Fundraising Expansion planning Virtual CFO services allow the business to access this expertise without waiting until it is large enough to create a full-time executive position. Industry providers consistently position outsourced CFO support as a practical middle ground for businesses that need strategic financial leadership without the fixed cost of a full-time CFO. 3. Better Cash-Flow Management A profitable business can still face a cash crisis. Profit is an accounting result. Cash flow reflects whether the organisation has enough money available to pay employees, suppliers, lenders, taxes and operating expenses. An SME may report profits while experiencing weak cash flow because: Customers pay late Inventory moves slowly Loan repayments are high Advance payments to suppliers increase Capital expenditure absorbs cash Tax liabilities were not planned Owner withdrawals are excessive Sales growth requires more working capital A Virtual CFO can prepare rolling

AI-Powered Accounting in 2026: How Smart Businesses Are Reducing Costs and Improving Financial Accuracy

TL;DR What Business Owners Need to Know AI-powered accounting uses technologies such as machine learning, intelligent document processing and automated workflows to complete repetitive financial tasks more efficiently. Businesses can use it to: Extract information from invoices and receipts Categorise transactions Reconcile bank entries Identify unusual transactions Monitor receivables Prepare management reports Improve cash-flow visibility Reduce manual accounting work However, AI should not be allowed to make important financial, tax or compliance decisions without professional review. Its output depends heavily on the quality of the underlying data, system configuration and internal controls. The most effective model in 2026 is therefore not “AI instead of an accountant.” It is AI-supported accounting combined with qualified human judgment. What Is AI-Powered Accounting? AI-powered accounting refers to the use of artificial intelligence and automation within bookkeeping, reporting, reconciliation, compliance and financial-management workflows. Traditional accounting software usually follows fixed rules. A user enters information, selects a ledger and generates a report. AI-enabled systems can go further by recognising patterns, reading documents, recommending classifications and identifying unusual transactions. For example, an AI-enabled accounting system may: Read a supplier invoice. Extract the supplier name, GST details, invoice number and amount. Suggest the appropriate expense category. Compare the invoice with an existing purchase order. Check whether the invoice has already been entered. Flag inconsistencies for review. Prepare the transaction for approval. The Institute of Chartered Accountants of India recognises that AI is changing accounting workflows by automating routine work and allowing chartered accountants to spend more time on strategic and analytical responsibilities. ICAI’s AI resources also demonstrate use cases involving compliance automation, MIS reporting, financial analysis and document preparation. sses Are Adopting AI Accounting in 2026 Many growing businesses do not suffer from a lack of financial data. They suffer from data that is delayed, incomplete or difficult to interpret. A business may have sales records in one application, bank information in another, GST data in spreadsheets and outstanding-payment details in email conversations. By the time this information is consolidated, management may already be working with outdated figures. AI accounting automation addresses this gap by making financial processing faster and more continuous. The broader adoption environment is also changing. In June 2026, ICAI reported that it had trained more than 50,000 members in artificial intelligence and developed over 150 GPT-based tools for professional use. This indicates that AI adoption is becoming part of mainstream professional-accounting development rather than remaining an isolated technology experiment. eport from Google and the India SME Forum, based on a survey of 3,249 MSMEs, estimated that wider AI adoption could unlock more than US$490 billion in economic value for Indian MSMEs. The report also associated digital-technology adoption with stronger growth and projected that AI could improve business profitability by 30% to 35%. These are ecosystem-level estimates rather than guaranteed outcomes for an individual company, but they illustrate why AI adoption has become a board-level issue for SMEs. ered Accounting Reduces Business Costs AI does not reduce costs simply because software performs a task. Savings arise when automation removes repetitive work, prevents avoidable errors and gives decision-makers useful information sooner. 1. Automating Repetitive Data Entry Manual invoice and receipt entry consumes hours that finance employees could spend on reconciliation, analysis and collections. Intelligent document-processing tools can extract information such as: Invoice date Vendor name GSTIN Tax amount Total value Payment terms Purchase-order reference The system can then suggest an accounting category and route the transaction for approval. This does not eliminate the need for verification. It reduces the amount of information that must be typed manually. 2. Accelerating Bank Reconciliation Traditional bank reconciliation requires employees to compare bank-statement entries with accounting records. An AI-enabled system can recommend matches based on: Amount Date Customer or vendor name Invoice reference Historical payment pattern Transaction description The finance team then reviews unmatched or uncertain transactions instead of checking every entry individually. This shifts effort from routine matching to exception management. 3. Reducing Correction and Rework Costs An accounting error rarely affects only one ledger. An incorrectly recorded transaction can distort: GST calculations Expense classification Profit margins Cash-flow reports Outstanding balances Management decisions Tax computations AI can flag duplicate invoices, unusual amounts, missing information and transactions that do not match historical patterns. Detecting the issue near the time of entry is usually less expensive than correcting several reports later. 4. Improving Receivables Management Businesses frequently focus on revenue without monitoring how quickly that revenue becomes cash. AI can help identify: Overdue customer balances Customers whose payment behaviour is deteriorating Invoices likely to be delayed Accounts requiring immediate follow-up Changes in average collection periods This helps the business prioritise collections instead of sending identical reminders to every customer. 5. Making Finance Teams More Productive Automation does not necessarily mean reducing the finance team. It can allow the same team to manage a larger transaction volume while spending more time on: Budgeting Cash-flow planning Cost analysis Margin review Vendor negotiations Management reporting Financial controls The real gain is not merely fewer working hours. It is a better allocation of professional time. How AI Improves Financial Accuracy Automated Document Extraction Manual typing creates opportunities for transposed digits, missed tax amounts and incorrect invoice references. Document-extraction systems can capture the original information directly from source documents. Employees only need to review fields that the system marks as uncertain. Duplicate and Anomaly Detection AI systems can compare new transactions against historical records and identify: Duplicate invoice numbers Repeated payment amounts Unusual vendor activity Unexpected changes in expense levels Transactions outside normal business hours Payments inconsistent with prior patterns These alerts do not prove that fraud or error has occurred. They help the reviewer decide where to investigate. Continuous Reconciliation Businesses that reconcile accounts only at month-end may discover problems several weeks after they occurred. Automated reconciliation enables more frequent comparison among: Bank records Sales invoices Purchase records Payment gateways Expense platforms Accounting ledgers More frequent reconciliation creates cleaner records and reduces the pressure associated with closing the books. Consistent Transaction Classification Humans may

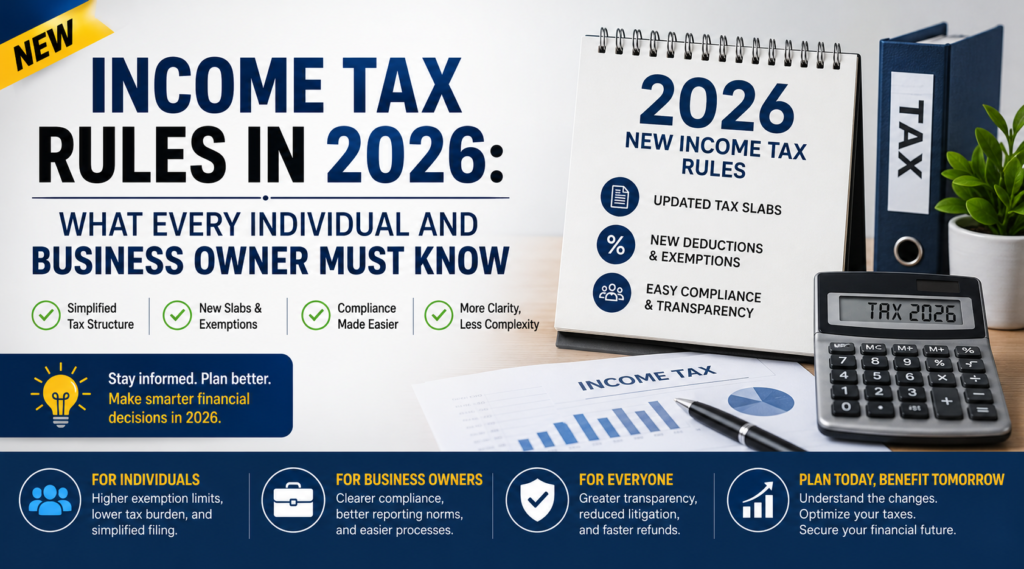

New Income Tax Rules in 2026: What Every Individual and Business Owner Must Know

TL;DR The Most Important 2026 Tax Changes India entered a major income-tax transition on April 1, 2026, when the Income-tax Act, 2025 came into force. Here is what taxpayers need to understand: The new Act applies to income earned from April 1, 2026 onward. The expression “Tax Year” now replaces the older concept of “Previous Year.” Returns for income earned between April 1, 2025 and March 31, 2026 are still filed for Assessment Year 2026–27 under the Income-tax Act, 1961. The new Act primarily simplifies and reorganises tax law; it did not itself introduce major changes to individual tax rates. The new tax regime continues as the default regime for eligible individual taxpayers. Under the new regime applicable to FY 2025–26 income, resident individuals may receive a rebate resulting in nil tax on normal income up to ₹12 lakh, subject to eligibility and exclusions. Salaried taxpayers may have no tax liability on salary income up to ₹12.75 lakh after the ₹75,000 standard deduction, where the applicable conditions are satisfied. ITR-1 and ITR-2 taxpayers generally continue with a July 31 filing timeline. Non-audit business cases have been moved to a later filing window, generally August 31. Payroll, TDS, advance-tax and accounting systems should now reference the Income-tax Act, 2025 for Tax Year 2026–27 transactions. The most important practical lesson is this: do not treat AY 2026–27 and Tax Year 2026–27 as the same compliance period. Why 2026 Is a Transition Year for Indian Taxpayers The year 2026 involves two income-tax frameworks operating side by side. Taxpayers filing their returns for income earned during FY 2025–26 must still use the old Assessment Year framework. At the same time, income earned from April 1, 2026 is governed by the Income-tax Act, 2025. This overlap can create confusion for: Salaried individuals preparing Form 16 records Freelancers calculating advance tax Businesses deducting TDS Employers configuring payroll software Companies planning tax provisions Taxpayers selecting the correct payment category Professionals preparing returns for AY 2026–27 The Income Tax Department has clarified that AY 2026–27 and Tax Year 2026–27 represent separate obligations. For income earned in FY 2025–26, the taxpayer files a return for AY 2026–27 under the earlier framework. For income earned during FY 2026–27, the new Tax Year framework applies, although the return for that income will ordinarily be filed in 2027. Income-tax Act, 2025: What Changed on April 1, 2026? The Income-tax Act, 2025 replaced the Income-tax Act, 1961 for income arising from April 1, 2026 onward. The principal objective was to make direct-tax law clearer, shorter and easier to navigate. The government stated that the new legislation focused on textual and structural simplification rather than introducing major policy changes or changing tax rates merely through the new Act. Tax Year Replaces Previous Year The new Act introduces the expression “Tax Year.” A Tax Year is generally the 12-month period within a financial year in which income is earned. Therefore, income earned between April 1, 2026 and March 31, 2027 belongs to Tax Year 2026–27. This replaces the older “Previous Year” terminology. The change is intended to reduce the confusion created by using one year for earning income and another “Assessment Year” for filing and assessment purposes. Sections and References Have Changed Many familiar tax provisions now appear under different sections or schedules. For example, employers and payroll teams must update references used in: Investment declarations Salary tax calculations TDS working papers Employee communications Tax-policy documents Accounting and compliance software A deduction that was commonly identified by an old section number may now appear under a new section or schedule in the Income-tax Act, 2025. The underlying tax treatment may continue, but the legal reference can be different. What Has Not Fundamentally Changed? The new Act does not mean that every established income-tax rule has disappeared. The following core obligations continue: Maintaining records Deducting and depositing TDS Paying advance tax where applicable Paying self-assessment tax Filing returns Reporting income accurately Responding to notices Preserving supporting documents Following tax-audit and other compliance requirements where applicable The law has been reorganised, but taxpayers still need disciplined documentation and accurate reporting. AY 2026–27 vs Tax Year 2026–27 This distinction is central to understanding the new income tax rules in 2026. Particular AY 2026–27 Tax Year 2026–27 Income period April 1, 2025 to March 31, 2026 April 1, 2026 to March 31, 2027 Governing law Income-tax Act, 1961 Income-tax Act, 2025 Return filing period Primarily during 2026 Primarily during 2027 Return terminology Assessment Year Tax Year Tax payment reference Old Act for FY 2025–26 liability New Act for income and payments from April 2026 Key action now Prepare and file AY 2026–27 return Maintain records and pay applicable tax under the new framework A taxpayer filing an ITR in July or August 2026 may therefore still be filing under the old Act, even though the new Act has already come into force for current-year income. Income-Tax Slabs for Income Earned During FY 2025–26 The new tax regime remained the default regime for eligible individuals and certain other taxpayers for AY 2026–27. New-Regime Slabs for AY 2026–27 Total income slab Tax rate Up to ₹4,00,000 Nil ₹4,00,001 to ₹8,00,000 5% ₹8,00,001 to ₹12,00,000 10% ₹12,00,001 to ₹16,00,000 15% ₹16,00,001 to ₹20,00,000 20% ₹20,00,001 to ₹24,00,000 25% Above ₹24,00,000 30% Health and Education Cess and surcharge may apply in addition to the basic tax, depending on the taxpayer’s circumstances and income level. Nil Tax up to ₹12 Lakh Does Not Mean a ₹12 Lakh Basic Exemption This point is frequently misunderstood. Under the new regime, the basic nil-rate slab is ₹4 lakh. The effective nil-tax position up to ₹12 lakh for eligible resident individuals arises through a tax rebate. It does not mean that every type of income up to ₹12 lakh is automatically exempt. Special-rate income, such as certain capital gains, may not receive the same rebate treatment. Taxpayers with capital gains, virtual digital assets, foreign assets or other specialised income should calculate their liability separately. Salaried Taxpayers and

Expert Guide to Investor Readiness: Financial Documents Every Startup Must Prepare Before Funding

TL;DR Investors do not fund only ideas. They fund businesses that can prove traction, financial discipline, compliance readiness and scalable economics. Before approaching investors, startups should prepare investor readiness financial documents such as financial statements, monthly MIS, bank statements, revenue breakdowns, expense reports, burn-rate calculations, financial projections, cap table, GST returns, income tax filings, debt schedules and a clean data room. A strong pitch deck may start investor conversations, but clean financial documents help close them. Why Investor Readiness Starts Before the Pitch Deck Many founders spend weeks perfecting the pitch deck but ignore the financial back-end of the business. That creates problems later. Once an investor shows interest, the next stage is due diligence. At this stage, investors verify whether the numbers, compliance records, ownership structure and business claims are reliable. Investor due diligence in India commonly reviews areas such as legal structure, financials, IP, cap table, tax, HR, DPIIT status and commercial validation. For startups, this means one thing clearly: fundraising readiness is not only a presentation exercise. It is a documentation exercise. A startup with clean financial records gives investors confidence. A startup with missing GST returns, unclear revenue data, unreconciled bank accounts or a confusing cap table creates risk. What Is Investor Readiness? Investor readiness means a startup is financially, legally and operationally prepared for investor review. An investor-ready startup can clearly show: How much revenue it earns Where revenue comes from How much cash it burns every month How long the current runway is Whether taxes and GST are compliant Who owns what percentage of the company Whether books match bank statements Whether projections are realistic Whether liabilities are properly disclosed Whether documents are organised in a data room Investor readiness does not mean the startup must be profitable. Many funded startups are still loss-making. But the startup must be transparent, organised and financially explainable. Financial Documents Investors Usually Review 1. Historical Financial Statements Investors usually ask for historical financial statements to understand how the business has performed. Prepare: Profit and loss statement Balance sheet Cash flow statement Notes to accounts, where available Trial balance Ledger summaries Auditor reports, where applicable Due diligence checklists commonly include audited financial statements for the last 2–3 years, balance sheet, P&L, cash flow and notes to accounts. For early-stage startups with limited operating history, founders should still prepare clean unaudited management accounts. 2. Monthly MIS and Management Accounts Annual statements are not enough for investors. They also want to understand recent performance. Prepare monthly MIS reports covering: Revenue Gross margin Net profit or loss Cash balance Burn rate Runway Customer acquisition cost Average revenue per customer Receivables Payables Budget vs actual performance Monthly management accounts for the last 12–24 months are often requested because they show how founders actually monitor the business. A strong MIS tells investors that the startup is not guessing. It is tracking performance. 3. Bank Statements and Reconciliations Bank statements help investors verify revenue, expenses, funding inflows and cash position. Prepare: Bank statements for all operating accounts Bank reconciliation statements Details of cash deposits, if any Founder contribution records Investment inflow records Loan receipts and repayments Major vendor payments Salary payments Investors may ask for the last 12 months of bank statements for operating accounts. If bank balances do not match books, investors may question the reliability of accounts. 4. Revenue Breakdown and Customer Data Top-line revenue is not enough. Investors want to know the quality of revenue. Prepare revenue breakdown by: Customer Product or service line Geography Channel Monthly cohort One-time vs recurring revenue B2B vs B2C revenue Existing vs new customers A startup should also prepare: Top customer list Customer concentration risk Monthly recurring revenue, if applicable Churn rate, where applicable Sales pipeline Signed contracts or purchase orders This helps investors understand whether revenue is repeatable, diversified and scalable. 5. Expense, Burn Rate and Runway Reports For startups, profitability may not arrive immediately. That is why investors carefully review burn rate and runway. Prepare: Monthly operating expenses Fixed vs variable costs Payroll cost Marketing spend Technology cost Rent and admin expenses Founder salary Consultant or contractor payments Monthly burn rate Runway calculation Cost reduction plan, if needed Burn rate shows how much cash the startup spends every month. Runway shows how long the startup can operate before needing more capital. A founder who knows burn rate and runway clearly earns more investor confidence. 6. Financial Projections and Business Model Investors expect projections, but they do not expect fantasy numbers. Prepare a financial model covering: Revenue projections Cost assumptions Gross margin Operating expenses Hiring plan Marketing spend Cash flow forecast Break-even point Funding requirement Use of funds Scenario analysis A good model should include realistic assumptions. For example, instead of saying “we will grow 10x”, founders should explain what will drive growth: more sales team members, channel partners, marketing ROI, higher retention, product expansion or pricing improvement. Financial projections for 3–5 years are commonly reviewed during fundraising due diligence. 7. Cap Table and Shareholding Records A cap table shows who owns the company. Prepare: Current shareholding pattern Founder shareholding ESOP pool, if any Past investment details Convertible instruments SAFE/CCD/CCPS details, if applicable Share transfer records Valuation history Dilution impact after proposed round A messy cap table is a major red flag. Investors want clarity on ownership, rights and dilution. The cap table should match MCA records, board approvals, shareholder agreements and investment documents. 8. Tax, GST and Compliance Documents Tax and compliance records are a major part of investor readiness. Prepare: Income tax returns GST registration certificate GSTR-1 filings GSTR-3B filings GSTR-2B reconciliation TDS returns TDS challans Form 26AS/AIS review Tax audit report, if applicable ROC filings AOC-4 and MGT-7/MGT-7A, where applicable Board resolutions Statutory registers GST filings and income tax returns are commonly included in financial due diligence document lists. If a startup is not compliant, investors may delay funding until issues are corrected. 9. Debt, Loans and Liabilities Schedule Investors want to know what obligations already exist. Prepare: Bank loans NBFC

Why Successful Businesses Conduct Quarterly Financial Health Checks Instead of Annual Reviews

TL;DR Successful businesses do not wait until year-end to understand their financial position. They conduct quarterly financial health checks to review cash flow, profitability, receivables, GST, TDS, tax planning, expenses, debt and business growth readiness. Annual reviews are useful for statutory reporting, but they often identify problems too late. Quarterly reviews help business owners take corrective action while there is still time to protect profit, improve liquidity and reduce compliance risk. Why Annual Financial Reviews Are No Longer Enough Many businesses review their finances only at the end of the financial year. By then, most decisions have already been made. Expenses are already incurred, GST returns are already filed, receivables may already be overdue, and tax planning options may be limited. This is why annual reviews often become reactive. A quarterly financial health check gives business owners a practical control system. It helps them understand whether the business is healthy, under pressure, or moving toward risk. For SMEs, this matters even more because cash flow and working capital can change quickly. The Economic Survey 2025–26 highlighted that around ₹8.1 lakh crore was stuck in delayed MSME payments, showing how seriously delayed receivables can affect liquidity and growth. What Is a Quarterly Financial Health Check? A quarterly financial health check is a structured review of a business’s financial position every three months. It usually covers: Cash flow Profitability Gross margin Receivables and payables GST and TDS compliance Advance tax position Expense trends Debt obligations Balance sheet strength Budget vs actual performance Growth readiness A financial health check helps businesses assess performance through key financial metrics such as cash flow and profit margins, while regular checks improve control and help identify issues early. In simple terms, an annual review tells you what happened. A quarterly review helps you decide what to do next. Quarterly Review vs Annual Review: Key Difference Area Annual Review Quarterly Financial Health Check Timing Once a year Every 3 months Nature Mostly reactive Proactive Cash flow visibility Often delayed Updated regularly Tax planning Limited time to act Better time for correction GST/TDS issues Found late Detected earlier Expense control Year-end analysis Quarterly correction Receivables Often reviewed after delay Tracked before pressure builds Business decisions Based on past data Based on current performance Best for Statutory closing Management control and growth What Successful Businesses Review Every Quarter 1. Cash Flow and Working Capital Cash flow is the first sign of business health. A company may show profit in books but still struggle with vendor payments, salaries, GST dues or loan EMIs. This usually happens when cash is blocked in receivables, inventory, advances or poorly planned expenses. Quarterly review should check: Opening and closing bank balance Monthly cash inflow Monthly cash outflow GST and TDS payments Salary and vendor commitments Loan repayment schedule Emergency cash reserve Working capital gap A strong quarterly review helps business owners answer a simple question: Do we have enough cash for the next 90 days? 2. Profit Margins and Cost Trends Revenue growth is not always healthy growth. A business may increase sales but still earn lower profit because costs are rising faster than income. Quarterly reviews help detect this early. Review: Gross profit margin Net profit margin Direct cost movement Employee cost Rent and fixed overheads Marketing spend Finance cost Discount leakage Product/service-wise profitability For example, if revenue increased by 20% but net profit increased only by 5%, the business needs to check pricing, vendor costs, staff productivity or overhead control. 3. Debtors and Delayed Payments Delayed receivables are one of the biggest hidden risks for SMEs. A business may issue invoices on time but collect payments late. This blocks working capital and creates pressure during tax payments, vendor payments and salary cycles. Quarterly debtor review should include: Total outstanding receivables Debtors ageing: 0–30, 31–60, 61–90 and 90+ days High-risk customers Delayed payment pattern Follow-up status Credit terms Bad debt risk A business that tracks receivables quarterly can act before overdue invoices become serious cash flow problems. 4. GST, TDS and Tax Position Quarterly financial health checks should include compliance review. Important checks include: GSTR-1 vs books GSTR-3B vs books GSTR-2B reconciliation Input tax credit eligibility TDS deduction and deposit TDS return filing Advance tax estimate Expense classification Tax audit applicability Notices or portal alerts This is important because compliance errors often grow silently. If GST mismatch or TDS default is identified after 12 months, correction becomes harder and costlier. 5. Balance Sheet Strength Many business owners look only at profit and loss. Successful businesses also review the balance sheet. Quarterly balance sheet review should check: Loans and borrowings Debtors Creditors Inventory Fixed assets Capital introduced Owner withdrawals Statutory dues Advances Unsecured loans A weak balance sheet can affect funding, bank loans, investor confidence and business valuation. 6. Budget vs Actual Performance A quarterly review should compare planned numbers with actual performance. Check: Expected revenue vs actual revenue Budgeted expense vs actual expense Planned profit vs actual profit Expected cash flow vs actual cash flow Projected GST/tax outflow vs actual liability Planned hiring vs actual payroll cost This helps business owners understand where plans are working and where correction is needed. 7. Business Growth Readiness A business should not expand only because sales are rising. Growth must be financially sustainable. Quarterly reviews help assess: Can the business afford expansion? Is cash flow stable? Are margins strong enough? Are books updated? Are tax compliances clean? Are reports investor-ready? Can the business take a loan safely? Is the current structure suitable for scale? This is where Virtual CFO support becomes valuable. A CA-led Virtual CFO review can convert accounting data into financial strategy. Step-by-Step Quarterly Financial Health Check Framework Step 1: Close Books Monthly Quarterly review is only useful if books are updated. Before review, ensure: Sales are recorded Purchases are entered Bank accounts are reconciled Expenses are classified GST data is updated TDS records are maintained Payroll entries are completed Step 2: Prepare Core Reports Prepare these reports: Profit and loss statement Balance

How Businesses in Chandigarh Can Reduce Tax Risks Through Better Financial Planning

TL;DR Businesses in Chandigarh can reduce tax risks by planning finances throughout the year instead of reacting during filing season. The most effective steps include monthly bookkeeping, GST reconciliation, TDS review, advance tax planning, expense documentation, cash flow forecasting and quarterly CA-led financial reviews. Tax risk usually does not appear suddenly. It builds slowly through missed entries, wrong classifications, delayed filings, poor documentation and weak financial controls. Why Tax Risk Is a Financial Planning Problem Many business owners treat tax risk as a filing issue. In reality, most tax problems begin much earlier. A wrong invoice, missed GST reconciliation, unpaid TDS, unsupported expense, delayed bookkeeping or poor cash flow plan can later become an income tax notice, GST mismatch, interest liability or penalty exposure. Better financial planning helps businesses: Estimate tax liability early Avoid last-minute cash pressure Claim eligible deductions correctly Maintain clean records Reduce GST and TDS mismatches Prepare for audit or scrutiny Make better business decisions For SMEs, startups and service businesses in Chandigarh, tax planning should be connected with accounting, GST, cash flow and compliance review. What Creates Tax Risk for Businesses? Tax risk usually comes from weak financial systems rather than one major mistake. Common causes include: Books updated only at year-end GST returns filed without reconciliation GSTR-2B mismatches ignored TDS deducted late or not deposited Advance tax not estimated properly Personal and business expenses mixed Cash transactions not reviewed Missing invoices and agreements Wrong expense classification Difference between GST turnover and income tax turnover No quarterly review by a CA Once these issues accumulate, correction becomes harder. Financial Planning Steps That Reduce Tax Risk 1. Maintain Accurate Monthly Books Clean books are the foundation of tax risk reduction. Monthly accounting should include: Sales entries Purchase entries Expense records Bank reconciliation Customer ledgers Vendor ledgers Loan accounts Fixed asset records GST and TDS entries Payroll records If books are updated only before filing, errors may remain hidden for months. Monthly books help identify gaps early and support better tax estimates. For example, if expenses are wrongly classified as capital or revenue items, the tax impact can change. A monthly review reduces such errors before year-end. 2. Reconcile GST Before Filing Returns GST mismatch is one of the most common tax-risk areas for Indian businesses. Businesses should reconcile: Record What to Check Sales register Invoice value, GSTIN, tax rate, place of supply GSTR-1 Outward supplies reported correctly GSTR-3B Tax liability paid correctly GSTR-2B Eligible input tax credit reflected Books of accounts Entries match return data E-invoices IRN and invoice values match, where applicable Filing GST without reconciliation can lead to ITC issues, notices and cash flow impact. GST portal changes and technical issues can also create compliance pressure, making early filing and review important. 3. Review TDS Applicability and Deposits TDS compliance is often missed when payments are made in a hurry. Businesses should review TDS on: Professional fees Contractor payments Rent Salary Interest Commission Certain purchase transactions Other specified payments The risk is not only late deposit. Incorrect TDS can affect expense allowance, vendor reconciliation and Form 26AS/AIS matching. A monthly TDS review should check: Whether TDS is applicable Correct section and rate PAN availability Timely deposit Quarterly return filing TDS certificate issuance 4. Plan Advance Tax Quarterly Advance tax planning prevents year-end pressure. Businesses should estimate: Quarterly profit Non-business income Capital gains, if any Deductions TDS already deducted Expected tax liability Cash available for tax payments Tax planning helps reduce liability legally, improves cash flow and reduces financial risk. A business that reviews advance tax quarterly avoids sudden March payments and interest exposure. 5. Separate Personal and Business Expenses Mixing personal and business expenses creates tax risk. Common examples include: Personal travel paid through business account Family expenses booked as business expenses Owner withdrawals not recorded properly Personal loans mixed with business funds Unsupported cash payments Better process: Maintain separate business bank account Record owner withdrawals separately Keep invoices for business expenses Document business purpose Review related-party transactions This improves audit readiness and reduces disallowance risk. 6. Maintain Strong Documentation Tax risk increases when claims cannot be supported. Businesses should maintain: Sales invoices Purchase bills Expense vouchers Agreements Bank statements Payment proofs GST returns TDS challans Payroll records Loan documents Fixed asset invoices Board resolutions, where applicable Good documentation protects the business during notices, audits and assessments. 7. Review Cash Flow Before Tax Due Dates Many businesses know tax is payable but do not plan cash flow for it. A tax cash flow plan should include: GST payments TDS deposits Advance tax Income tax dues Professional tax/payroll-related dues, where applicable ROC and annual compliance fees Audit and filing costs This avoids emergency borrowing and missed due dates. 8. Conduct Quarterly CA-Led Reviews Quarterly reviews help reduce tax risk before it becomes expensive. A CA-led quarterly review should cover: Profit and loss review Balance sheet review GST reconciliation TDS compliance Advance tax estimate Receivables and payables Cash flow forecast Expense classification Tax-saving opportunities Notice or portal alerts For growing businesses, Virtual CFO support can also help convert accounting data into cash flow planning, profitability tracking and tax-risk management. Tax Risk Reduction Checklist Area Review Frequency Risk Reduced Bookkeeping Monthly Wrong profit, missed expenses GST reconciliation Monthly ITC mismatch, notices TDS review Monthly/Quarterly Interest, disallowance Advance tax Quarterly Interest and cash pressure Expense documents Monthly Disallowance Cash flow Monthly Missed tax payments Balance sheet Quarterly Hidden liabilities CA review Quarterly Compliance and tax risk Common Mistakes Businesses Should Avoid Mistake 1: Tax Planning Only in March By March, most transactions are already complete. Quarterly planning gives more time to correct issues. Mistake 2: Filing GST Without GSTR-2B Review ITC should be checked against GSTR-2B before claiming. Vendor delays can affect credit. Mistake 3: Ignoring TDS Until Return Filing TDS should be reviewed at payment stage, not after the quarter ends. Mistake 4: Poor Documentation Even genuine expenses may be questioned if proof is missing. Mistake 5: Not Matching GST and Income Tax Turnover Turnover

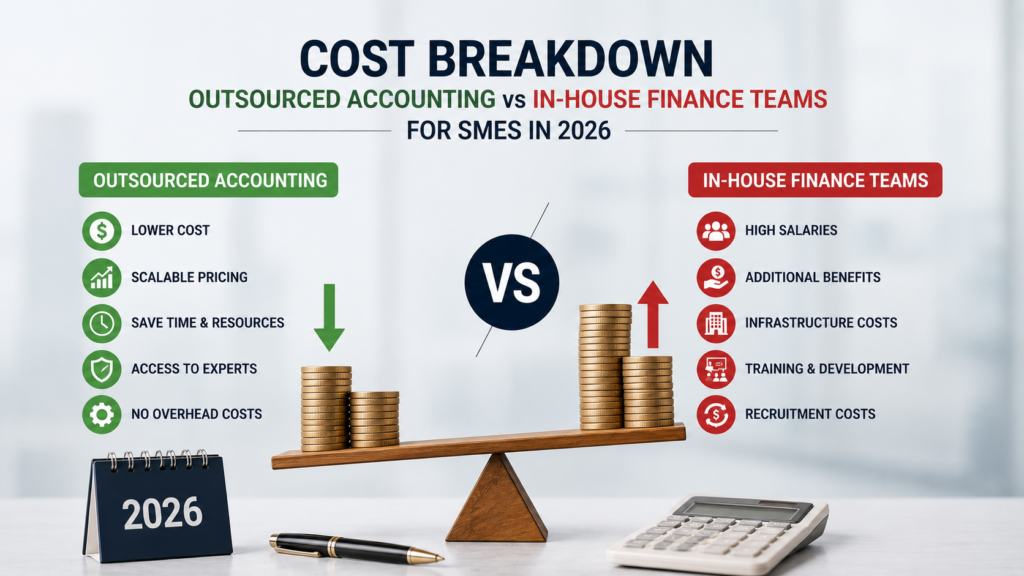

Cost Breakdown: Outsourced Accounting vs In-House Finance Teams for SMEs in 2026

TL;DR For many SMEs, outsourced accounting can be more cost-efficient than building a full in-house finance team, especially when the business needs bookkeeping, GST compliance, monthly reporting, payroll coordination, tax support and CA review without fixed salary burden. An in-house finance team gives control and daily availability, but it also brings salary, hiring, training, software, supervision, attrition and compliance risk costs. The best model for most growing SMEs in 2026 is not purely outsourced or purely in-house. It is a hybrid model: routine work supported by technology, outsourced CA-led review, and internal coordination where needed. Why SMEs Need to Compare the Real Cost, Not Just Salary Most business owners compare outsourced accounting with in-house finance by looking only at monthly salary. That creates an incomplete picture. The real cost of finance includes: Salaries Employer benefits Hiring time Training Accounting software GST and TDS compliance review Management reporting Senior finance supervision Staff attrition Error correction Penalty risk Business owner time For SMEs, finance is not only a back-office function. It affects tax planning, cash flow, vendor payments, receivables, GST credits, audit readiness and profitability. If the finance system is weak, the business may lose money even when sales are growing. What Is an In-House Finance Team? An in-house finance team means the business directly hires employees to manage accounts, bookkeeping, billing, payments, reconciliations, payroll support, GST data and reporting. A typical SME finance setup may include: Junior accountant Senior accountant Accounts executive Finance manager Payroll/accounting coordinator External CA for filings and audit For a very small business, one accountant may handle everything. But as transactions grow, one person is rarely enough. The challenge is that SMEs often hire a junior accountant and expect them to manage bookkeeping, GST, TDS, MIS, payroll, compliance and advisory. This creates dependency and increases error risk. What Is Outsourced Accounting? Outsourced accounting means the business assigns accounting, bookkeeping, reporting and compliance support to an external professional firm or CA-led team. Depending on scope, outsourced accounting may include: Bookkeeping Bank reconciliation Sales and purchase accounting Expense recording GST data preparation GSTR-2B reconciliation support TDS working Payroll coordination MIS reporting Vendor/customer ledger review Monthly closing Financial statements CA review Virtual CFO support CA Rohit Jain’s service mix includes accounting, bookkeeping, GST, audit, corporate finance and Virtual CFO services, making outsourced accounting suitable for SMEs that need both execution and professional review. Cost Comparison Table: Outsourced vs In-House Finance Cost Area In-House Finance Team Outsourced Accounting Monthly salary Fixed salary cost Fixed or flexible service fee Hiring cost Recruitment time and cost No direct hiring burden Training Business must train staff Provider brings process expertise Software Business pays separately May use shared or recommended systems Supervision Owner/manager must review CA-led review may be included GST/TDS compliance Needs expert oversight Can be built into service scope Scalability Need more hires as work grows Scope can increase gradually Attrition risk High dependency on staff Lower dependency on one employee Reporting quality Depends on employee skill Depends on service scope and review quality Strategic finance Usually missing unless senior hire Can add Virtual CFO support Hidden Costs of an In-House Finance Team 1. Salary and Benefits The visible cost of an in-house finance team is salary. But salary alone is not the full cost. Businesses may also pay: Employer contributions Bonuses Leave salary Laptop and workspace cost Software access HR/admin time Replacement cost during attrition A finance manager in India can cost significantly more than a junior accountant. Glassdoor’s June 2026 estimate shows average accounting and finance manager salary in India around ₹14.32 lakh per year, with a typical range from about ₹9.97 lakh to ₹18.68 lakh annually. This does not include every overhead a business may incur. For SMEs, this fixed cost becomes heavy if the finance workload does not justify a full senior team. 2. Hiring and Training Hiring finance staff is not only about posting a job. The business must spend time on: Screening candidates Interviews Salary negotiation Onboarding Training on business process Explaining GST/accounting workflow Reviewing early mistakes Replacing staff if they leave If the business owner personally supervises the accountant, that time has a cost. 3. Software and Technology Modern finance teams need accounting software, cloud storage, payroll systems, billing tools, GST utilities and reporting dashboards. Software costs may include: Accounting software subscription GST reconciliation tools Payroll software Cloud storage Data backup Cybersecurity controls User access management If software is not set up properly, the business may still face errors despite paying for tools. 4. Supervision and Review An accountant records transactions. But someone must review whether the records are correct. This includes: GST reconciliation TDS applicability Expense classification Balance sheet review Vendor/customer ledgers Cash and bank reconciliation Profitability reports Audit readiness If a business hires only a junior accountant, professional review is still needed. Without review, errors may remain hidden until filing, audit or tax notice stage. 5. Compliance Risk Compliance mistakes can become more expensive than salary. Common risks include: Wrong GST rate Missed ITC reconciliation Late GST return filing TDS deduction errors Incorrect expense booking Poor documentation Mismatch between books and returns Delayed financial statements Weak audit records An in-house team without CA-level review can create hidden risk. What Outsourced Accounting Usually Includes Outsourced accounting services can be customised, but a strong SME package usually includes: Monthly bookkeeping Bank reconciliation Purchase and sales accounting GST working and reconciliation TDS working Monthly closing Accounts receivable tracking Accounts payable tracking Expense classification MIS reports Periodic CA review Compliance calendar support Audit coordination Tax planning inputs Virtual CFO add-on, where required This allows SMEs to access a broader skill set without hiring separate people for every function. When In-House Finance Makes Sense In-house finance may be better when: The business has very high daily transaction volume Multiple departments need real-time finance support Inventory and billing operations are complex Internal approvals need constant coordination Data confidentiality requires tight internal control The business can afford a structured finance department There is a senior finance leader available internally For

Startup Compliance Guide 2026: Everything New Businesses in Chandigarh Need to Know

TL;DR Startup compliance in Chandigarh is not limited to company registration. A new business must plan its legal structure, PAN, TAN, GST registration, accounting system, income tax, TDS, ROC filings, payroll, contracts, DPIIT recognition and investor documentation from the beginning. The biggest mistake founders make is treating compliance as an afterthought. In 2026, clean records and timely filings are essential for credibility, funding, tax safety and sustainable growth. Why Startup Compliance Matters from Day One Many founders focus only on product, sales, hiring and marketing during the early stage. That is understandable, but ignoring compliance can become expensive later. A startup may look small in the first few months, but every decision creates a compliance impact: Which structure should the business use? Should the startup register for GST? Is TAN required for TDS? Are contracts properly documented? Are books maintained monthly? Is the company filing ROC forms on time? Is investor documentation ready? Can the business claim Startup India benefits? For new businesses in Chandigarh, compliance is not just a legal requirement. It is a growth foundation. Banks, investors, customers and vendors all trust businesses that maintain clean statutory records. Startup Compliance Checklist for Chandigarh Businesses 1. Choose the Right Business Structure The first compliance decision is choosing the right structure. Common options include: Business Structure Best For Key Compliance Level Proprietorship Small individual businesses Low Partnership Firm Small businesses with partners Moderate LLP Professional/service businesses with limited liability Moderate Private Limited Company Startups seeking funding, scale and credibility Higher OPC Solo founder businesses needing corporate identity Moderate A private limited company may be preferred for startups planning funding, ESOPs, investors or scalable operations. LLPs may suit service-based businesses that want limited liability with relatively simpler compliance. The wrong structure can create tax, compliance and funding problems later. Before registration, founders should review ownership, liability, tax impact, investor plans and long-term goals with a CA. 2. Complete Business Registration Once the structure is selected, complete registration properly. For a private limited company, this may include: Name approval DSC for directors DIN-related compliance SPICe+ incorporation filing MOA and AOA Certificate of Incorporation PAN and TAN allotment Registered office documentation For LLPs, compliance may include: Name reservation Digital signatures LLP incorporation filing LLP agreement PAN and TAN Registered office proof A startup should ensure that founder names, shareholding, capital structure, registered office and business objects are correctly documented at the start. 3. Apply for PAN, TAN and Bank Account PAN is essential for tax filings, bank accounts, invoices and financial transactions. TAN is required when the business deducts TDS. Startups should also open a dedicated business bank account. Mixing personal and business transactions creates accounting confusion and weakens tax documentation. Early finance setup should include: Business bank account PAN and TAN records Authorised signatory details Digital signature management Accounting software setup Invoice format Document storage system This creates a clean base for future tax and compliance work. 4. Check GST Registration Applicability GST registration is one of the most important startup compliance decisions. In general, GST registration becomes mandatory when a business crosses prescribed turnover thresholds. Current GST guidance indicates that goods suppliers in most normal category states generally follow the ₹40 lakh threshold, while service providers generally follow the ₹20 lakh threshold. Some special category rules and compulsory registration cases may apply. Startups should also review GST registration if they: Sell goods or services across states Sell through e-commerce platforms Need to issue GST invoices to B2B customers Want to claim input tax credit Provide taxable services Deal with corporate clients requiring GST invoices GST compliance includes: GSTR-1 GSTR-3B GSTR-2B reconciliation E-invoicing applicability review Input tax credit tracking Tax invoice compliance GST payment planning A startup should not wait until turnover crosses the threshold if customers, contracts or business model require GST registration earlier. 5. Maintain Proper Books of Accounts Accounting is not only for filing returns. It helps founders understand whether the business is actually profitable. Startups should maintain: Sales register Purchase register Expense records Bank reconciliation Fixed asset records Loan records Founder contribution records Customer and vendor ledgers GST and TDS workings Payroll records Poor bookkeeping creates problems during tax filing, funding rounds, bank loan applications and due diligence. A monthly accounting process is better than year-end clean-up because errors are easier to correct early. 6. Track Income Tax and Advance Tax Startups must plan income tax from the beginning. Important areas include: Correct profit calculation Expense classification Depreciation Advance tax estimation Capital expenditure review Founder remuneration Director payments Related-party transactions Tax audit applicability ITR filing If a startup becomes profitable, advance tax may apply. Waiting until year-end can create interest and cash flow pressure. Startups should review tax position at least quarterly. 7. Manage TDS Compliance TDS is often missed by new businesses. Startups may need to deduct TDS on: Salary Professional fees Contractor payments Rent Commission Interest Certain high-value transactions TDS compliance includes deduction, deposit, return filing and certificate issuance. If TDS is not handled correctly, expenses may face disallowance and the startup may incur interest or penalties. A simple TDS tracker should be maintained from the first month. 8. Complete ROC and MCA Compliance Private limited companies and LLPs must follow MCA/ROC compliance. For private limited companies, annual compliance generally includes financial statement filing and annual return filing. AOC-4 is generally filed within 30 days of the AGM, while MGT-7 is generally filed within 60 days of the AGM. Important company compliance may include: Board meetings AGM Statutory registers Financial statements Director disclosures Auditor appointment AOC-4 filing MGT-7 / MGT-7A filing ITR filing Event-based filings for changes For LLPs, annual compliance generally includes LLP annual return and statement of accounts/solvency filings. Startups should not ignore ROC filings even if there is no revenue. Compliance still applies once the entity is incorporated. 9. Apply for DPIIT Startup Recognition DPIIT recognition under Startup India can help eligible startups access benefits such as tax benefits, easier compliance, IPR fast-tracking and related startup ecosystem support. Startup India states that